Last year, the WBCSD (World Council for Sustainable Business Development), headed by the fearless Peter Bakker, published a review of sustainability reporting called Reporting Matters. I didn't get to blog about it at the time (I wish I could do nothing but blog) but I have taken it up again in the run-up to the invitation-only WBCSD Council Meeting in a couple of weeks in Atlanta, where I will be speaking and moderating in some sessions. The Atlanta meeting is themed: "Business - Setting the Pace". At this meeting, with the belief that business is a driving force for delivering sustainable solutions to the world’s most pressing challenges, senior executives of WBCSD member companies come together to explore opportunities to advance WBCSD's Action2020 strategy. The Council Meeting draws CEOs, Council Members and thought leaders from across all sectors and geographies in a high-level game-changing outcome-oriented week of debates and decisions.

For those not familiar with WBCSD, it is an organization with a powerful voice in our sustainability landscape and a leading authority on natural and social capital risk management, disclosure and valuation. I include a brief blurb from the WBCSD website.

"The WBCSD is a CEO-led organization of forward-thinking companies that galvanizes the global business community to create a sustainable future for business, society and the environment.

From its starting point in 1992 to the present day, the Council has created respected thought leadership on business and sustainability.

The Council plays the leading advocacy role for business. Leveraging strong relationships with stakeholders, it helps drive debate and policy change in favor of sustainable development solutions.

The Council provides a forum for its 200 member companies - who represent all business sectors, all continents and combined revenue of over $US 7 trillion - to share best practices on sustainable development issues and to develop innovative tools that change the status quo. The Council also benefits from a network of 60 national and regional business councils and partner organizations, a majority of which are based in developing countries.

By thinking ahead, advocating for progress and delivering results, the WBCSD both increases the impact of our members’ individual actions and catalyzes collective action that can change the future of our society for the better."

Now you know. Check out the website. It's a wealth of resources.

Now you know. Check out the website. It's a wealth of resources.

Anyway, back to the matter in hand and that's Reporting Matters. (Matter, matters. Good, right ?)

WBCSD produced this report in partnership with communications consultancy Radley Yeldar as a tool to help improve the effectiveness of reporting. Member companies can use the WBCSD analysis of their reporting to help improve different aspects of their own disclosure. Reporting Matters 2013 the baseline report and the research is ongoing with reports planned to be published annually. In early November, in Atlanta, the new Reporting Matters 2014 will be presented to give an updated view of data and trends in reporting effectiveness.

Peter Bakker introduced the 2013 baseline report with the words (among others): "We believe that reporting practices need

to change to ensure that businesses are

truly valued on what is important, that

stakeholders have timely information, and

that reports are read and used by investors

and other stakeholders."

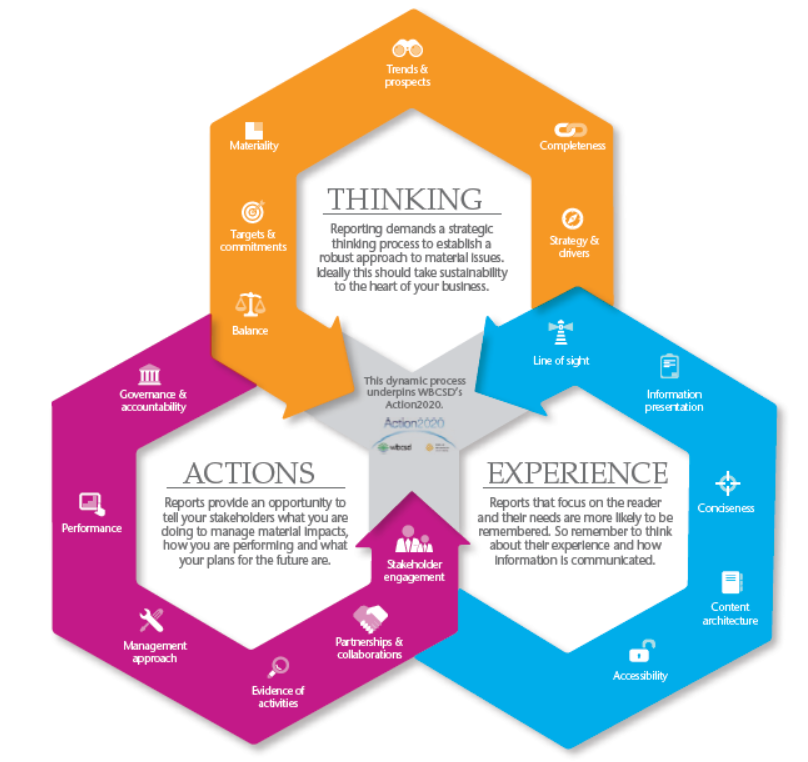

Reporting Matters measures the effectiveness of corporate sustainability reporting and to do so, it defines an effectiveness framework based on three key elements: The Thinking that defines the report, the Actions (relating to material impacts) that the report discloses and the Experience that the reader has when reading the report.

The Reporting Matters baseline examined 175 Sustainability Reports (including integrated reports) of WBSCD member companies across 20 sectors and 30 countries against 17 criteria (12 content-related and 5 experience-related).

For each of these criteria, Reporting Matters explains the approach, provides key findings from the research, offers recommendations and showcases best practice distilled from the 175 reports analyzed. Some of the overarching conclusions were:

- Companies are reporting far more than a focus on material impacts might suggest. This makes for long, unwieldy reports and difficulty in finding the most relevant and useful information.

- When combined with the annual report, the amount of sustainability content disclosed is generally less than a standalone report.

- 75% of the reports analyzed follow GRI Guidelines and these tended to be the ones with the higher effectiveness scores.

- 80% of the 175 reports analyzed were standalone sustainability reports. However, self-declared integrated reports scored higher on the WBCSD effectiveness scale than many standalones.

- 60% of companies have some form of external assurance at some level on some part of the report but only 4 companies (2%) used reasonable assurance for their entire report.

But the real meaty stuff of this report is in the detailed analysis of the report against the stated criteria. Unfortunately, WBCSD does not share with us, the general professional public, the exact scores that each report received (though WBCSD member companies each receive their own scores and have the opportunity to discuss and review with WBCSD Reporting Matters experts). However, Reporting Matters shares enough for us to get the benefit of the learning and appreciate some great examples of reporting practice. Some examples follow.

Strategy and Drivers: Reporting Matters says: "A sustainability strategy is a clearly-articulated approach or plan to address material

financial, environmental, social and governance risks and opportunities. It should

link to a vision, a mission and provide an explanation of how the strategy will be

delivered, including milestones and targets."

This made me stop and think, and agree, as more and more, I find that I read sustainability reports with a need to understand the strategic relevance and embedded approach that companies have adopted. In the early days of reporting, it was all about taking action in addition to doing your business. Reports were all about "we did this" and "we did that", where "this" and "that" referred to a volunteering activity, a charitable donation, a training event for employees or a LED lighting retrofit. No connection to an overall approach, strategic direction or business relevance other than the platitudes of "giving back", "doing the right thing" and "valuing our planet". Today, it's about being accountable for impacts across the value chain and through the core business. Today, if sustainability is not part of your business strategy, then your business strategy is not part of your future success. In any sustainable business strategy there is value, and that value should be clear as we read a company's sustainability report. Reporting Matters found that:

This made me stop and think, and agree, as more and more, I find that I read sustainability reports with a need to understand the strategic relevance and embedded approach that companies have adopted. In the early days of reporting, it was all about taking action in addition to doing your business. Reports were all about "we did this" and "we did that", where "this" and "that" referred to a volunteering activity, a charitable donation, a training event for employees or a LED lighting retrofit. No connection to an overall approach, strategic direction or business relevance other than the platitudes of "giving back", "doing the right thing" and "valuing our planet". Today, it's about being accountable for impacts across the value chain and through the core business. Today, if sustainability is not part of your business strategy, then your business strategy is not part of your future success. In any sustainable business strategy there is value, and that value should be clear as we read a company's sustainability report. Reporting Matters found that:

- The most effective reporters disclose a business strategy that links to positive sustainability outcomes, such as the management or avoidance of sustainability risks or the development of opportunities through innovation. The strategy is supported by a detailed implementation plan.

- The most effective reporters define a specific business case for sustainability, referencing drivers such as cost savings, reputational benefits, and employee retention, as well as wider societal needs.

- Many reporters however do not establish a clear link between sustainability and their core business nor do they define a company-specific business case.

- Many reports do not include a sustainability vision and consequently do not communicate a clear sense of direction or purpose.

Svenska Cellulosa is a global hygiene and forest products company with around 44,000 employees that develops and produces sustainable personal care, tissue and forest products. The current Svenska Report for 2013 supports the insights noted by Reporting Matters about the prior report. Often, you can tell how much sustainability is embedded in a company's strategy simply by looking at what the company chooses to highlight. In 2013, Svenska highlighted real business developments that have sustainable value.

While Svenska links its activities to business drivers and reports the results of activities, there is room to go further by reporting more outcomes and linking these outcomes to the business, as well as social and environmental value created.

Evidence of Activities: Reporting Matters says: "Evidence of activities involves reporting on sustainability activities such as strategic

programs and initiatives that occur during the reporting year, or progress of

existing sustainability activities. It helps link management approaches to actions

and performance and can substantiate statements and claims."

Well, evidence of activities may not seem too much of a stretch for most reporters. In fact, most reporters are more than happy to elaborate on things they did. I wonder if the focus here shouldn't be more on evidence of outcomes rather than activities. However, Reporting Matters 2013 made some relevant recommendations for reporters that refer to the way outcomes are included in disclosures.

Well, evidence of activities may not seem too much of a stretch for most reporters. In fact, most reporters are more than happy to elaborate on things they did. I wonder if the focus here shouldn't be more on evidence of outcomes rather than activities. However, Reporting Matters 2013 made some relevant recommendations for reporters that refer to the way outcomes are included in disclosures.

- Include more specific narrative on strategic sustainability activities that address material issues during the reporting year.

- Illustrate sustainability activities through relevant and compelling case studies focusing on material issues, linked to a wider strategic program or management action and focused on outcomes.

- Provide appropriate background on the development of strategic programs and initiatives over time but focus on achievements and progress during the reporting year.

- Show how disclosed management processes and tools support the implementation of strategic programs and initiatives.

This is sustainable core business, and references the difference (outcome) that Lafarge is making through sustainable innovation. I would welcome even more detail on the actual outcomes in case studies such as these, but in general, this is an effective way to get the message through.

Partnerships and Collaborations: Reporting Matters says: "Appropriate and strategic partnerships and collaborations can help accelerate action

and scale up solutions by combining expertise, resources and networks across key

stakeholders who share a common goal. Partnerships and collaborations should

focus on addressing a company’s material issues and support the implementation

of a company’s sustainability strategy."

This is an interesting criterion and one that is becoming more imperative for most companies as we speak. More and more, the revelation that collaboration is key to sustainability is affecting the way companies approach their own strategies and actions. Our client, Netafim, who recently published a Sustainability Report called "At the Heart of the Food, Water and Land Nexus", knows only too well that, just as all problems are interdependent, so are all solutions. Collaboration is therefore part of the solution. Where every material impact is at some form of nexus (my new sustainability buzzword), so every material action is also at some form of nexus. Collaboration at the Nexus - that's our future.

Reporting Matters 2013 shared these key findings:

This is an interesting criterion and one that is becoming more imperative for most companies as we speak. More and more, the revelation that collaboration is key to sustainability is affecting the way companies approach their own strategies and actions. Our client, Netafim, who recently published a Sustainability Report called "At the Heart of the Food, Water and Land Nexus", knows only too well that, just as all problems are interdependent, so are all solutions. Collaboration is therefore part of the solution. Where every material impact is at some form of nexus (my new sustainability buzzword), so every material action is also at some form of nexus. Collaboration at the Nexus - that's our future.

Reporting Matters 2013 shared these key findings:

- The most effective reporters highlight strategic partnerships and collaborations that address material issues, and help to implement the company’s sustainability strategy.

- The most engaging reports provide details on the expected benefits of partnerships and collaborations for the business as well as for relevant stakeholders.

- Companies however do not always consistently focus on establishing partnerships which are strategic and that have the potential to deliver the biggest value for the business by being closely aligned with the overall sustainability strategy. Such partnerships are typically philanthropic and not linked to core strategy.

One of the three showcased examples of Partnerships and Collaborations is the Vodafone plc 2012/2013 report which Reporting Matters says has a strong partnership-oriented focus.

I checked out Vodafone plc's 2013/2014 Sustainability Report and this continues to play out. The word "partnership" features more than 50 times in this report and it's choc with partnership examples in the area of core business. These include partnership around e-mobility, M2M connectivity, technology-supported waste management, smart working solutions, women's security, sustainable agriculture and many more examples.

I could go on (a lot) but I think this post is already long enough. The point is simply that Reporting Matters is an exceptionally useful document that helps us understand some of the ways in which reporting can become more effective, which according to the WBCSD approach means that it demonstrates strategic sustainability thinking and actions leading to materially relevant outcomes while being focused, balanced and engaging to read.

There are a couple of aspects relating to reporting that I might have added to the WBCSD effective-reporting criteria. There are some things I always look for that for me, really make the difference to the effectiveness and quality of a sustainability report. For example, the leadership statement. This is not directly covered by the defined Reporting Matters criteria. Interestingly too, because WBCSD is a "CEO-led" organization. The CEO statement in any report should not be just an evergreen boilerplaty platitudy we-love-ourselves cringe-piece. It should add value to the report by clearly framing the report context, the company strategic focus and challenges and the intentions to deliver improved material impacts on stakeholders. The CEO statement is the entrance-lobby of the report. If it's not compelling, you don't want to go any further.

Having said that, WBSCD seems to have a good recipe. What makes it truly worthwhile is the ongoing nature of this analysis. The 2013 report is interesting, but the trends and dynamics that will be observed over time with each successive report are the key. It'll be fascinating to see how things have changed during the past year. While we shouldn't get carried away and expect complete transformation of reporting in such a short time, the introduction of G4, the new IIRC framework, progress in SASB standards development, CDP expansion, consultations by WBCSD with its reporting member companies and a generally highly dynamic reporting environment with increasingly legislative orientation (such as the recent European directive) and greater SEC commitment (e.g. Singapore), it's possible that we might find that reporting effectiveness has turned up a notch.

But Reporting Matters 2014 is not the only reason I am looking forward to being in Atlanta. Guess what else I found to do.

There are a couple of aspects relating to reporting that I might have added to the WBCSD effective-reporting criteria. There are some things I always look for that for me, really make the difference to the effectiveness and quality of a sustainability report. For example, the leadership statement. This is not directly covered by the defined Reporting Matters criteria. Interestingly too, because WBCSD is a "CEO-led" organization. The CEO statement in any report should not be just an evergreen boilerplaty platitudy we-love-ourselves cringe-piece. It should add value to the report by clearly framing the report context, the company strategic focus and challenges and the intentions to deliver improved material impacts on stakeholders. The CEO statement is the entrance-lobby of the report. If it's not compelling, you don't want to go any further.

Having said that, WBSCD seems to have a good recipe. What makes it truly worthwhile is the ongoing nature of this analysis. The 2013 report is interesting, but the trends and dynamics that will be observed over time with each successive report are the key. It'll be fascinating to see how things have changed during the past year. While we shouldn't get carried away and expect complete transformation of reporting in such a short time, the introduction of G4, the new IIRC framework, progress in SASB standards development, CDP expansion, consultations by WBCSD with its reporting member companies and a generally highly dynamic reporting environment with increasingly legislative orientation (such as the recent European directive) and greater SEC commitment (e.g. Singapore), it's possible that we might find that reporting effectiveness has turned up a notch.

But Reporting Matters 2014 is not the only reason I am looking forward to being in Atlanta. Guess what else I found to do.

elaine cohen, CSR consultant, Sustainability Reporter, HR Professional, Ice Cream Addict. Author of Understanding G4: the Concise guide to Next Generation Sustainability Reporting AND Sustainability Reporting for SMEs: Competitive Advantage Through Transparency AND CSR for HR: A necessary partnership for advancing responsible business practices . Contact me via Twitter (@elainecohen) or via my business website www.b-yond.biz (Beyond Business Ltd, an inspired CSR consulting and Sustainability Reporting firm). Check out our G4 Report Expert Analysis Service - for published G4 reports or pre-publication - write to Elaine at info@b-yond.biz to help make your G4 reporting even better.

No comments:

Post a Comment