I have often said that business is done in sectors. A sector-based approach offers a platform for developing a shared appreciation of sustainability opportunities, risks, benefits and challenges while providing leverage for change and a support network for non-competitive knowledge sharing. Last month, I was delighted to engage with the Oil and Gas Industry for a day of working together all about sustainability reporting. I was able to share insights, recommendations and an external perspective while gaining a deeper understanding of the constraints and considerations that reporting specialists share in the large, complex, established companies in this industry, most of which have been reporting for years. For me, this was both an enriching experience and an opportunity to help.

My reporting day was hosted as part of an annual meeting of members of IPIECA - the global oil and gas industry association for environmental and social issues. IPIECA was formed in 1974 following the launch of the United Nations Environment Programme (UNEP). IPIECA is the only global association involving both the upstream and downstream oil and gas industry on environmental and social issues. IPIECA’s membership covers over half of the world’s oil production.

The core of IPIECA's mission and practical agenda is the development of the sector as a social and environmentally responsible player. IPIECA's most recent publication a couple of months ago was the Third Edition of Sustainability Reporting Guidance for the Oil and Gas Industry to help companies report across the industry's most common sustainability issues in a consistent way and in line with shared stakeholder expectations.

The 180 page volume of guidance draws on several years of reporting experience in the sector and external independent stakeholder input. It covers both the reporting process (and principles) and reporting guidance including what's material for Oil and Gas. The principles are simply stated: relevance, transparency, consistency, completeness and accuracy.

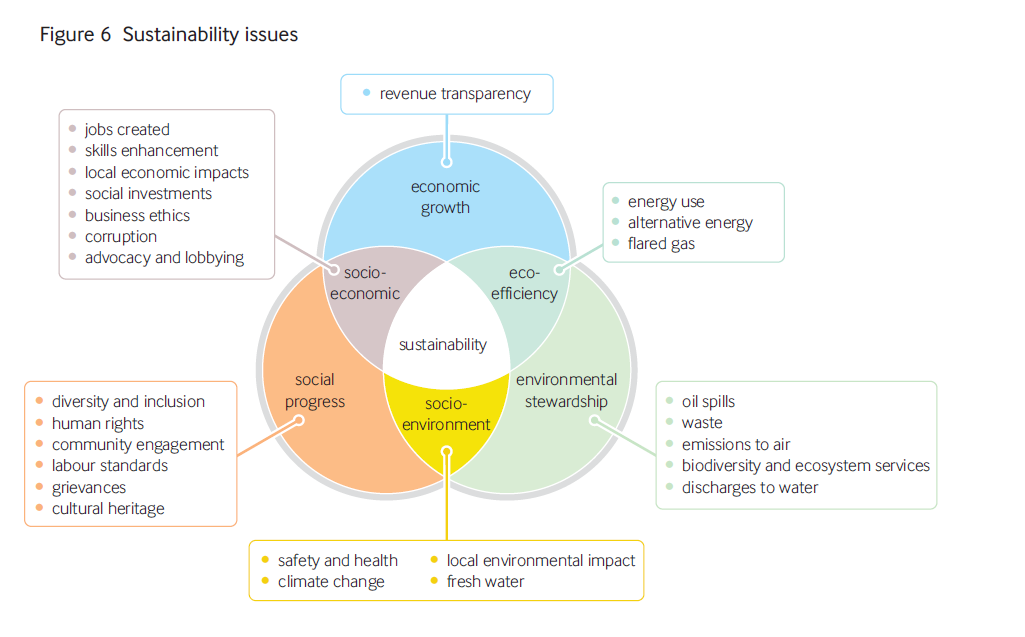

The IPIECA guidance also suggests a set of the most significant issues commonly associated with the oil and gas industry, broadly referring to types of sustainability aspects, including

risks, impacts and benefits, related to the life cycle and value chain of a company’s activities.

The IPIECA guidance also suggests a set of the most significant issues commonly associated with the oil and gas industry, broadly referring to types of sustainability aspects, including

risks, impacts and benefits, related to the life cycle and value chain of a company’s activities.

But then... the reporting guidance makes a distinction between three types of reporting elements: the common ones... that means, essentially, there's no point in producing a report unless you include these; the supplemental ones, that means, basically, a good selection of your peers probably already report so you should consider including if you want to be at the top of the game and finally, others. Others is what differentiates you.

And here is an example I prepared earlier:

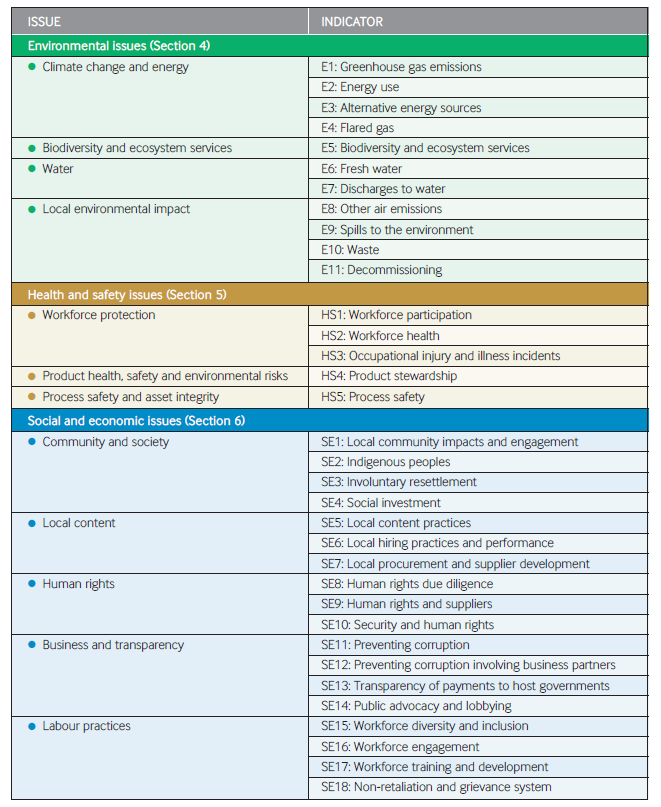

So E1 - greenhouse gas emissions - actually becomes 10 separate indicators, some of which are very specifically tailored to the oil and gas industry. Ultimately, it's not so different from the GRI approach, where performance indicators are grouped into categories and aspects. IPIECA has selected 34 aspects for its member reporters - GRI G4 as you may recall has 46 aspects. Many companies in this sector choose to report GRI as well as being guided by IPIECA, and a cross-reference of the different performance indicators in each framework is provided.

The IPIECA approach makes for a simple and straightforward content index - see this one in Chevron's 2014 report - it is somewhat less cumbersome than a full GRI Content Index as the sub-indicators - the different reporting elements - are not identified in the index.

I think it's a great thing that a sector proactively provides guidance and comprehensive tools for the member companies. It's more than just guidance - it's a demonstration of accountability for driving the sector forward with a shared expectation around sustainability practice and transparency. The value of the debate in developing the framework, the value of the learning in applying the reporting guidance and the value of reviewing the challenges of reporting are immense. That's how it seemed to me in my working day with many companies from the Oil and Gas industry, including sustainability reporting representatives of BG Group, BP, Chevron, ConocoPhillips, ExxonMobil, Hess Corporation, Marathon Oil, Noble Energy, OMV, Repsol, Shell, Statoil, Total and Tullow Oil.

In our workshop day, we discussed three aspects of reporting that are always fascinating:

elaine cohen, CSR consultant, Sustainability Reporter, HR Professional, Ice Cream Addict. Author of Understanding G4: the Concise Guide to Next Generation Sustainability Reporting AND Sustainability Reporting for SMEs: Competitive Advantage Through Transparency AND CSR for HR: A necessary partnership for advancing responsible business practices . Contact me via Twitter (@elainecohen) or via my business website www.b-yond.biz (Beyond Business Ltd, an inspired CSR consulting and Sustainability Reporting firm). Need help writing your first / next Sustainability Report? Contact elaine: info@b-yond.biz

The core of IPIECA's mission and practical agenda is the development of the sector as a social and environmentally responsible player. IPIECA's most recent publication a couple of months ago was the Third Edition of Sustainability Reporting Guidance for the Oil and Gas Industry to help companies report across the industry's most common sustainability issues in a consistent way and in line with shared stakeholder expectations.

The 180 page volume of guidance draws on several years of reporting experience in the sector and external independent stakeholder input. It covers both the reporting process (and principles) and reporting guidance including what's material for Oil and Gas. The principles are simply stated: relevance, transparency, consistency, completeness and accuracy.

The IPIECA reporting guidance suggests a list of 34 performance indicators that are likely to be relevant to companies reporting in this sector. Fairly straightforward - 11 greenie ones, 5 health and safety, and 18 across workplace and community.

But then... the reporting guidance makes a distinction between three types of reporting elements: the common ones... that means, essentially, there's no point in producing a report unless you include these; the supplemental ones, that means, basically, a good selection of your peers probably already report so you should consider including if you want to be at the top of the game and finally, others. Others is what differentiates you.

And here is an example I prepared earlier:

So E1 - greenhouse gas emissions - actually becomes 10 separate indicators, some of which are very specifically tailored to the oil and gas industry. Ultimately, it's not so different from the GRI approach, where performance indicators are grouped into categories and aspects. IPIECA has selected 34 aspects for its member reporters - GRI G4 as you may recall has 46 aspects. Many companies in this sector choose to report GRI as well as being guided by IPIECA, and a cross-reference of the different performance indicators in each framework is provided.

The IPIECA approach makes for a simple and straightforward content index - see this one in Chevron's 2014 report - it is somewhat less cumbersome than a full GRI Content Index as the sub-indicators - the different reporting elements - are not identified in the index.

I think it's a great thing that a sector proactively provides guidance and comprehensive tools for the member companies. It's more than just guidance - it's a demonstration of accountability for driving the sector forward with a shared expectation around sustainability practice and transparency. The value of the debate in developing the framework, the value of the learning in applying the reporting guidance and the value of reviewing the challenges of reporting are immense. That's how it seemed to me in my working day with many companies from the Oil and Gas industry, including sustainability reporting representatives of BG Group, BP, Chevron, ConocoPhillips, ExxonMobil, Hess Corporation, Marathon Oil, Noble Energy, OMV, Repsol, Shell, Statoil, Total and Tullow Oil.

In our workshop day, we discussed three aspects of reporting that are always fascinating:

- planning the reporting process

- defining and reporting materiality

- reporting climate change

And while I am not able to disclose the details of the discussions that took place throughout the day, I did receive permission to share a small selection of the closing insights that the 25 or so people in the room shared at the end of the day.

10: Prioritizing material issues: Care needs to be taken when prioritizing material issues - it's not always as straightforward as it might seem. Overly mechanical formulas or highly detailed positioning of issues on a matrix may not be as valuable as the time invested. Not every material issue is more or less important than other issues. Sometimes they are the same. There also needs to be a balance in reporting to ensure that issues that are not identified as most material are not completely omitted as some stakeholders may require these.

9: Additional resources: You don't have to cram everything into your report. In some cases, supplementary content can be added as an appendix or a web-page. Not everything needs to be upfront narrative.

8: Less is more: (ha ha, no further comment)

7: Tighten the timeline: In the oil and gas industry, companies are very large and complex and global data collection takes the time that it takes. Often this, together with other reporting considerations, can drag out the reporting timeline across several months - in a survey of IPIECA member companies before the workshop, we discovered that the average reporting cycle was more than 8 months. If you are reporting annually, this doesn't leave too much time to go to the beach. I am pretty clear on this. Any report that takes more than 6 months to prepare from concept to publication is taking too long. And that's generous. While there are often practical considerations that delay the publication of the report, the more you can compact the timeline, the more time you have for making progress rather than making reporting.

6: Give up the search for the perfect formula: This is so true. In preparation for my work with the sector, I reviewed 15 Oil and Gas Sustainability Reports from 2014. Despite the fact that all these companies are in the same industry, the reports all have their individual character, style, tone and content focus. Each company is at a different stage of development along the sustainability journey. So, while I was able to share insights on the different ways of defining, prioritizing and presenting material issues, and participants took away new ideas, one size does not fit all and there is absolutely no perfect reporting formula for all organizations, only one for each organization.

5: Balance the broad and the narrow: It's important to find a middle ground between reporting at a broad level about complex issues versus increasing the resolution to report at a more granular level on specific issues. How do you represent that your overall carbon footprint reduction is made up of a thousand small actions and impacts, and which of those, if any, are worth highlighting? This is something worth thinking about as you plan your report process and content.

4: Get the design right: Everyone would agree that content precedes design. If you don't have relevant content, even the best of designers will fail to make your report credible. Yet, getting the design right for your corporate culture and sustainability content can make the report come alive in ways that words alone cannot. Careful use of infographics, any photography other than stock photography and controlled use of colors, fonts and styles will only improve the appeal and readability of your report.

3: Stakeholders were not all born equal: Don't let individual stakeholder groups dominate your content and do map and prioritize your stakeholders in advance and decide what you need from them and how you will represent their voices in your report. Giving stakeholders a voice - letting them tell your story - is often a proven route to credibility.

2: Link materiality to metrics: How many reports, especially with the fuller adoption of G4, now include a materiality matrix or list of material impacts. Yes, most or all. How many create a clear linkage (I call this the "materiality audit trail") between what's stated as material and all the rest of the report content - performance indicators, case studies, policy narrative etc? Oops. Rather few. So often, there is a gaping dissonance between what the report says it should be about and what it actually includes. But getting this alignment is not enough. The report user should be able to easily and quickly find the link between material impact and reporting content about that impact. I generally apply the "ten-minute rule" - if I can't find something after ten minutes of trying, for me, it doesn't exist. We have to make the link between materiality, content and metrics both available and quick to locate.

1: Have confidence: It's tempting to get derailed in reporting - there are so many frameworks, guidelines and complex rules and requirements that you can spend forever questioning yourself on the right way to go and the best way to pull it all together. But this can lead to a spiral of indecision that can delay the report process and dilute the content. Often the best way is simply to make your selection of how to frame and develop your report, and then have confidence in your approach and make it happen. No-one knows what you might have done. Everyone sees what you do. Best feel good about it and present it with pride. There are no bad Sustainability Reports. There are only Sustainability Reports that can help us improve our sustainability performance and disclosure. Each report is a learning platform, but it's also an achievement to be proud of.

And one more insight from me:

Even though we didn't have ice cream throughout this day-long meeting :-), it was one of the best sustainability days I have had in a while: a dialogue with like-minded professionals who are eager to do their honest best for their company, society and planet. I didn't even miss the ice cream!

9: Additional resources: You don't have to cram everything into your report. In some cases, supplementary content can be added as an appendix or a web-page. Not everything needs to be upfront narrative.

8: Less is more: (ha ha, no further comment)

7: Tighten the timeline: In the oil and gas industry, companies are very large and complex and global data collection takes the time that it takes. Often this, together with other reporting considerations, can drag out the reporting timeline across several months - in a survey of IPIECA member companies before the workshop, we discovered that the average reporting cycle was more than 8 months. If you are reporting annually, this doesn't leave too much time to go to the beach. I am pretty clear on this. Any report that takes more than 6 months to prepare from concept to publication is taking too long. And that's generous. While there are often practical considerations that delay the publication of the report, the more you can compact the timeline, the more time you have for making progress rather than making reporting.

6: Give up the search for the perfect formula: This is so true. In preparation for my work with the sector, I reviewed 15 Oil and Gas Sustainability Reports from 2014. Despite the fact that all these companies are in the same industry, the reports all have their individual character, style, tone and content focus. Each company is at a different stage of development along the sustainability journey. So, while I was able to share insights on the different ways of defining, prioritizing and presenting material issues, and participants took away new ideas, one size does not fit all and there is absolutely no perfect reporting formula for all organizations, only one for each organization.

5: Balance the broad and the narrow: It's important to find a middle ground between reporting at a broad level about complex issues versus increasing the resolution to report at a more granular level on specific issues. How do you represent that your overall carbon footprint reduction is made up of a thousand small actions and impacts, and which of those, if any, are worth highlighting? This is something worth thinking about as you plan your report process and content.

4: Get the design right: Everyone would agree that content precedes design. If you don't have relevant content, even the best of designers will fail to make your report credible. Yet, getting the design right for your corporate culture and sustainability content can make the report come alive in ways that words alone cannot. Careful use of infographics, any photography other than stock photography and controlled use of colors, fonts and styles will only improve the appeal and readability of your report.

3: Stakeholders were not all born equal: Don't let individual stakeholder groups dominate your content and do map and prioritize your stakeholders in advance and decide what you need from them and how you will represent their voices in your report. Giving stakeholders a voice - letting them tell your story - is often a proven route to credibility.

2: Link materiality to metrics: How many reports, especially with the fuller adoption of G4, now include a materiality matrix or list of material impacts. Yes, most or all. How many create a clear linkage (I call this the "materiality audit trail") between what's stated as material and all the rest of the report content - performance indicators, case studies, policy narrative etc? Oops. Rather few. So often, there is a gaping dissonance between what the report says it should be about and what it actually includes. But getting this alignment is not enough. The report user should be able to easily and quickly find the link between material impact and reporting content about that impact. I generally apply the "ten-minute rule" - if I can't find something after ten minutes of trying, for me, it doesn't exist. We have to make the link between materiality, content and metrics both available and quick to locate.

1: Have confidence: It's tempting to get derailed in reporting - there are so many frameworks, guidelines and complex rules and requirements that you can spend forever questioning yourself on the right way to go and the best way to pull it all together. But this can lead to a spiral of indecision that can delay the report process and dilute the content. Often the best way is simply to make your selection of how to frame and develop your report, and then have confidence in your approach and make it happen. No-one knows what you might have done. Everyone sees what you do. Best feel good about it and present it with pride. There are no bad Sustainability Reports. There are only Sustainability Reports that can help us improve our sustainability performance and disclosure. Each report is a learning platform, but it's also an achievement to be proud of.

And one more insight from me:

Even though we didn't have ice cream throughout this day-long meeting :-), it was one of the best sustainability days I have had in a while: a dialogue with like-minded professionals who are eager to do their honest best for their company, society and planet. I didn't even miss the ice cream!

Very interesting, Elaine! One quick follow-up question: in the GHG emissions reporting guidance, I don't see anything about comparing emissions to the carbon budget -- which is really the primary reason for reporting GHG emissions in the first place. Am I missing something? Or does IPIECA really leave this integral step out of the mix? If so, the implications are profound! I know you've written elsewhere on your blog on the importance of reporting impacts within the context of ecological limits (ie your piece on the uselessness of materiality matrices), so I wonder when the reporting world is going to catch up with this necessary practice...

ReplyDeletehi Bill, thanks for reading and for your comments about reporting and the carbon budget. As always, an interesting observation. Best, Elaine

ReplyDeleteThanks Elaine -- so am I correct in assuming that the IPIECA guidance does not call for budget-based accounting of carbon? As you likely know, the corporate world is heading toward science-based targets (see for example http://www.sciencebasedtargets.org/ ), so IPIECA seems to be lagging on this front. I would be very interested to hear a more expansive explanation of your perspective on this. Thanks!

ReplyDeleteHi again Bill, yes, I understand the move toward science-based targets. I am looking forward to a transformational outcome of COP21 to provide, among other things, a framework for companies around the world to operate within. I believe the issue of climate change reqires a collective response that goes beyond the specific reporting practice of any single company or sector.

ReplyDeleteHey Elaine -- thanks for your response -- I agree that a global framework for reporting GHG emissions in the context of science-based thresholds (eg 2 degrees / 350ppm / carbon budget) is the best way forward. GRI's SustyContext Principle provides the conceptual underpinning, and the WWF / WRI / CDP / UNGC Science-Based Targets initiative provides methodologies. It would have been helpful if the IPIECA had stepped up to provide industry-endorsed guidance on this vital issue, but it appears that this is not the case. And I'm not aware of a specific agenda item at COP21 on creating such a global framework that you suggest -- let's let each other know about it if we hear anything :-)

ReplyDeleteHope to see you at the GRI Conference!

Best,

Bill