One of the things that appears challenging for many reporters in G4 requirements to define material Aspect Boundaries. I just had a query on that this week from another consultant who is working an a client G4 report. Here are the GRI disclosure requirements:

When you get past the techno-babble, you can see that reporters are asked to state the locations where material impacts occur. It's fairly easy to assume what was in the minds of the GRI G4 designers when they put this together. It's like this. Not all impacts are equal, and not all impacts are relevant to all parts of an organization. Some have an impact outside the organization, and, taking a value chain approach to sustainability, it's important to identify where your organization is accountable even though it is not directly in control. The GRI FAQ states: "Listing entities outside of the organization where impacts related to material Aspects occur, is the

first step for reporters to show that they are aware of these impacts in their value chain."

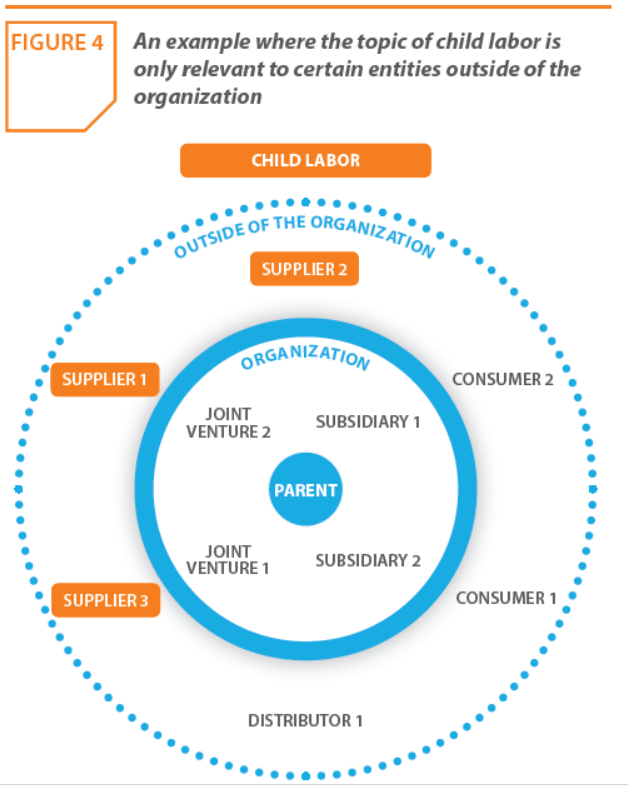

One of a few examples in the G4 implementation manual refers, for example, to child labor in the supply chain.

One of a few examples in the G4 implementation manual refers, for example, to child labor in the supply chain.

While child labor may be strictly controlled in direct company operations, it's much harder to control in the supply chain and the relevant material impact may be pinpointed there. The G4 expectation, therefore, is that companies would specifically identify impacts that occur outside the organization as well as inside, making a distinction between the two, so that stakeholders can be appropriately informed.

At some level, this makes sense. It's part of the G4 transformation that requires companies to actually think about their material issues rather than auto-list boilerplate issues that mean everything to everybody. Now, reporters should think about who is affected outside the factory gate as well. Companies which analyze their material issues right down to specific localized impacts will probably have a better foundation for addressing the risks of such issues and engaging more closely with local stakeholders to inform a strategic approach.

However, this is proving to be rather challenging for many large reporters at a global level. Responses to G4-20 and G4-21 are lacking depth and showing signs of box-ticking in a way that undermines the true value of this kind of disclosure. Remember that the Aspect Boundary relates to a material Aspect, and each material Aspect requires a DMA - a disclosure on management approach describing why the Aspect is material and what the organization is doing about it. G4-20 and G4-21 are effectively extensions of the descriptions of the most material issues.

Material issues are not that simple, however. Almost every material issue that has an external impact also has an internal one and vice versa. Companies are having a hard time understanding the distinction between the two. The default seems to be that everything impacts everything and everybody and all company entities are affected. In G4-21, there is also a requirement to state the geographical location where external impacts occur. Well. GRI might just have suggested an auto-response for this. The Universe.

Material issues are not that simple, however. Almost every material issue that has an external impact also has an internal one and vice versa. Companies are having a hard time understanding the distinction between the two. The default seems to be that everything impacts everything and everybody and all company entities are affected. In G4-21, there is also a requirement to state the geographical location where external impacts occur. Well. GRI might just have suggested an auto-response for this. The Universe.

Insurance company Metlife's G4 2013 Corporate Responsibility report was just published. Take a look Metlife's response to G4-201 and G4-21 to a some of their material issues.

As you can see, everything is both material internally and externally and impacting pretty much everyone everywhere. Stakeholder groups (not entities) have been noted against each issue. Entities have not been stated so we can assume everything applies to the entire organization.

It's not so easy to define where impacts occur. Employment and diversity are noted as only material internally. However, in some cases, with large companies, the impact of a diverse employment policy can be quite significant in local communities. Many of the decisions taken in the Human Resources Department have broadly-felt impacts on society. Check out my book, CSR for HR. The stakeholder view of people management goes way beyond the impacts felt inside the organization. Metlife confirms this in the DMA for this diversity:

The impact of a diverse organization is also felt at the level of customers and in communities. With operations around the world, and more than 65,000 employees, perhaps Metlife's hiring and inclusion policies are having an impact at local level. Or maybe not materially so. It's an interesting thought - one that is probably answered through engagement with local stakeholders.

What about public policy? Metlife calls this both an internal and an external impact. I can understand the external part. In the DMA, Metlife writes:

This seems to indicate that the impact is external, rather than internal. So where is the internal impact? Could it be that engaging in public policy requires an internal effort by the organization to understand and maintain positions on public policy, ensure staff are appropriately trained, manage the internal adjustments required as a result of regulatory changes etc? Could it be the effect on profit of political donations? It's possible. But Metlife has not mentioned this internal impact in its narrative, focusing on the external impacts of regulation. The performance indicator supporting this material issue that Metlife reports is G4-S06 which relates to the number of political donations made - maybe this is then both internal (expenditure/profit) and external (political influence). Either way, deciding the exact Aspect Boundary of this material Aspect is not so straightforward.

Metlife is not the only one....

Banco Santander in its G4 Comprehensive report for 2013 report adds a nice little matrix (it's in Portuguese but we'll get the gist).

Everything is material internally and externally (red triangles) , with the exception of the positive impacts of the bank on society (black circle) - indirect economic impacts and local community impacts. These are not considered to have an internal impact. In addition, in the report's GRI Content Index, Banco Santander notes different stakeholder groups that are affected by the different impacts. But no differentiation is made between entities and no geographic location is mentioned. Oh, and this report was verified by Deloitte.

Dow Chemicals in its G4 comprehensive 2013 Annual Sustainability Report also has a nice little matrix. Dow is a global company with 53,000 people and products manufactured in 201 sites in 63 countries. Try breaking down Aspect Boundaries for each of those entities.

At Dow, then, all material impacts are internally material. Only three material impacts are external as well, affecting broader society - product safety, health and environment protection and community success. Issues such as water, sustainable agriculture and climate change are not noted as materially important outside the organization. I wonder how this analysis was performed and how material issues such as climate change and sustainable agriculture are not considered to be material externally. Oh, and this report was verified by ERM.

H&M Conscious Actions 2013 Sustainability Report fares no better on G4-20 and G4-21. The response to these disclosures is a webpage. But the webpage is the GRI index page. So you get into a G4-20 G4-21 loop - and you never get to the actual disclosure. That's one way of avoiding having to think about this rather messy disclosure conundrum.

Oh, and the H&M report was verified by Ernst and Young.

CVS Caremark's 2013 CSR Report includes a little more detail in this table contained in the content index. It clearly states that internal issues relate to all CVS Caremark's operations in the U.S. and that externally material issues are predominantly in the supply chain in China. This is getting closer to the G4-20 and G4-21 requirement.

But, with 19 material issues, this summary goes only part way to fully providing the Aspect Boundaries for each material Aspect. Also, in all the external issues reported, the company is noted as one of the affected stakeholders. But the company is an internal stakeholder. Hmm. A bit confusing.

GRI's own G4 report has a fairly clear approach. Although geographic locations are not noted, there are some explanations as to what's material to whom. Most of the material impacts occur both externally and internally.

Overall, then, I am not finding responses to G4 Aspect Boundaries especially helpful in many of the G4 reports I have reviewed so far. I think this just as much a flaw of the framework as it is with reporters who can't be bothered to think about this more meaningfully or simply don't know how to respond.

The idea is good.

Companies should identify how and where their operations are impacting external stakeholders.

It's quite simple really.

But, the roundabout rather convoluted GRI-techno-babble of G4-20 and G4-21 dumbfounds companies and is leading to a bunch of stilted and meaningless disclosures. It's also dumbfounding report assurers - all of whom confirm that reports are in accordance when these basic general disclosures are not adequately reported.

In G5, maybe it would be simpler to have just one disclosure. Forget internal impacts. Everything the company externally does affects it internally one way or another. There's not much point in stating that everything affects employees.

My suggestion:

G5-20: State how and where your business activities materially affect external stakeholders throughout your value chain.

Voila! Plain, simple, clear, helpful and tecnhobabbly-challenged.

No?

elaine cohen, CSR consultant, Sustainability Reporter, HR Professional, Ice Cream Addict. Author of Understanding G4: the Concise guide to Next Generation Sustainability Reporting AND Sustainability Reporting for SMEs: Competitive Advantage Through Transparency AND CSR for HR: A necessary partnership for advancing responsible business practices . Contact me via www.twitter.com/elainecohen or via my business website www.b-yond.biz (Beyond Business Ltd, an inspired CSR consulting and Sustainability Reporting firm). Check out our G4 Report Expert Analysis Service - for published G4 reports or pre-publication - write to Elaine at info@b-yond.biz to help make your G4 reporting even better.

No comments:

Post a Comment