Earlier this year, I had quite a lot of fun as a GRI-appointed Quality Control Officer, whose role is to attend GRI training courses as an observer and report back to GRI if certified GRI training is being conducted professionally, competently and in line with GRI standards. This is fascinating for me, mainly because it's so interesting to hear what training delegates ask about and comment on during the course. In one session, a delegate asked the ultimate G4 (now GRI Standards) question - the very same one that I asked GRI Standards leading architect Bastian Buck of GRI, three years back:

Is it OK to write a G4 report with just one material issue?

The answer of course is Yes and No.

Yes, because technically, if you have determined that your organization has only one material impact, then disclosing this and using GRI to report it does actually tick the box.

No, because, I believe, no organization can be so simple that its impact is entirely mono-dimensional. Even micro-businesses operate across more than one dimension. No business has just one stakeholder.

Behind this ultimate question, then, is the deeper consideration of how organizations define their most material impacts for the purpose of strategy development and reporting. It's not so much about whether you can ride the framework with one material issue; it's about the value you derive from understanding what's material for your business.

Materiality and Strategy

One of the positive developments following the introduction of G4 was the elevation of materiality from dormant to active in the minds of companies and reporters. Transitioning to G4 has generally appeared to cause companies to engage in some level of thinking about what's material and how to define it. In some cases, this has been a meaningful exercise where materiality is the result of insightful stakeholder dialogue and the precursor to a multi-year sustainability strategy and basis for reporting. In other cases, we are still seeing the disconnect - where companies have, on the one hand, a sustainability strategy and, on the other hand, a list of material issues that bears no resemblance to the strategy and a report which covers everything except what is deemed material. The next stage in materiality maturity is helping companies to see that this all plays out on the same playground. Sustainability strategy has to be the result of materiality analysis. Materiality can never be in a vacuum.

Materiality and Impacts

Which brings me to another interesting and highly geeky thing I did this week. I listened in on the GRI Global Sustainability Standards Board (GSSB) meeting (for the second time). It's fascinating to be a fly on the wall as the GSSB debates the different aspects of developing GRI Standards. I have to commend GRI and GSSB on full transparency here - all the meeting documents are available and the meeting itself is audio live-streamed (shame about the video!) - and it's a truly illuminating discussion... if you are a reporting geek like me.

One of the topics that came up this time around was the definition of materiality and the clarification of this in the new GRI Standards. GRI maintains that to date, people have "misinterpreted" the definition of materiality, and that the new terminology in GRI Standards makes this much clearer. GRI Standards 100:1.3 states: "Relevant topics, which potentially merit inclusion in the report, are those that can reasonably be considered important for reflecting the organization’s economic, environmental, and social impacts, or influencing the decisions of stakeholders. In this context, ‘impact’ refers to the effect an organization has on the economy, the environment, and/or society (positive or negative)."

In the GRI 100 Glossary of the GRI Standards, it is now clarified as follows:

In the GRI 100 Glossary of the GRI Standards, it is now clarified as follows:

A Sustainability Report should therefore report impacts OF the business and ON the decisions of stakeholders. It is not about the impacts of sustainability on the business. The guidance matrix in the GRI Standards remains the same in the GRI Standards is it was in G4 (though the colors have changed a little 😌) (NB: I remind you that a matrix is NOT necessary for GRI Reporting - a list of priority issues is perfectly adequate.)

A Sustainability Report should therefore report impacts OF the business and ON the decisions of stakeholders. It is not about the impacts of sustainability on the business. The guidance matrix in the GRI Standards remains the same in the GRI Standards is it was in G4 (though the colors have changed a little 😌) (NB: I remind you that a matrix is NOT necessary for GRI Reporting - a list of priority issues is perfectly adequate.)

This the application of this matrix - or specifically, the focus of each of the axes - has commonly been misused in G4 reporting.

This the application of this matrix - or specifically, the focus of each of the axes - has commonly been misused in G4 reporting.

3M's 2016 Sustainability Report, for example, uses reputation on the Y axis and stakeholders on the X axis:

The Fedex 2016 Global Citizenship Report uses stakeholders and business success:

The Fedex 2016 Global Citizenship Report uses stakeholders and business success:

Both these approaches do not reflect the actual intention of the GRI framework. The GRI approach is designed to create a report that reflects impacts on the economy, people and planet. The shape and size of the impact of your specific business is key to defining your positive (or negative) contribution to society. The primary focus in sustainability reporting should be the size and nature of the impacts OF your business and how your business affects our lives. In the GRI Standards, that should now be crystal clear. The outcomes of the way your business addresses mitigating negative impacts or enhancing positive impacts is reflected in your reputation, business success and value creation.

In the conversation at the GSSB, where I was a fly, a concern was raised that some companies have spent fortunes on materiality assessments that include this measure of "importance to business success". "What should they do now?", was the question. Well, it's not the end of the world. There is some overlap. Quite often, these issues will naturally coincide. Almost always, in fact. But in the next review of material impacts, there's an opportunity to better align with the letter and spirit of the reporting standard (and stakeholder expectations).

Which brings me to the more important question: How do you prioritize material impacts?

Materiality and Impacts

Which brings me to another interesting and highly geeky thing I did this week. I listened in on the GRI Global Sustainability Standards Board (GSSB) meeting (for the second time). It's fascinating to be a fly on the wall as the GSSB debates the different aspects of developing GRI Standards. I have to commend GRI and GSSB on full transparency here - all the meeting documents are available and the meeting itself is audio live-streamed (shame about the video!) - and it's a truly illuminating discussion... if you are a reporting geek like me.

One of the topics that came up this time around was the definition of materiality and the clarification of this in the new GRI Standards. GRI maintains that to date, people have "misinterpreted" the definition of materiality, and that the new terminology in GRI Standards makes this much clearer. GRI Standards 100:1.3 states: "Relevant topics, which potentially merit inclusion in the report, are those that can reasonably be considered important for reflecting the organization’s economic, environmental, and social impacts, or influencing the decisions of stakeholders. In this context, ‘impact’ refers to the effect an organization has on the economy, the environment, and/or society (positive or negative)."

In G4, material impacts were defined as follows:

3M's 2016 Sustainability Report, for example, uses reputation on the Y axis and stakeholders on the X axis:

Both these approaches do not reflect the actual intention of the GRI framework. The GRI approach is designed to create a report that reflects impacts on the economy, people and planet. The shape and size of the impact of your specific business is key to defining your positive (or negative) contribution to society. The primary focus in sustainability reporting should be the size and nature of the impacts OF your business and how your business affects our lives. In the GRI Standards, that should now be crystal clear. The outcomes of the way your business addresses mitigating negative impacts or enhancing positive impacts is reflected in your reputation, business success and value creation.

In the conversation at the GSSB, where I was a fly, a concern was raised that some companies have spent fortunes on materiality assessments that include this measure of "importance to business success". "What should they do now?", was the question. Well, it's not the end of the world. There is some overlap. Quite often, these issues will naturally coincide. Almost always, in fact. But in the next review of material impacts, there's an opportunity to better align with the letter and spirit of the reporting standard (and stakeholder expectations).

Which brings me to the more important question: How do you prioritize material impacts?

Materiality and Prioritization

The big weakness in the GRI Standards is the lack of robust guidance for defining the process for prioritizing material impacts. GRI could have been prescriptive in this area. The GRI Standards omit the guidance that was contained in G4 around the stages of defining material impacts: identification, prioritization, validation and review. However, even that guidance did not prescribe a robust process for getting from the universe of many impacts to the fewer most material impacts. Few companies, if any, actually report this process in a way that help us understand the voices that counted in prioritizing specific impacts.

It's easy enough to define the landscape of relevant issues. But the prioritization has often been reduced to a number-crunching exercise, where different groups give scores to different topics, the numbers are added up and voila - you have a matrix. The outcome of this process can vary widely depending on which voices you count, what weight you give to each voice, how each voice assesses the value of each impact and the weighting factors you use to roll that up into one coherent list of issues. These details are rarely disclosed by companies. The entire basis upon which material impact reporting rests is therefore not transparent and possibly, not robust.

Lloyds Bank publishes a Materiality Report.

It's easy enough to define the landscape of relevant issues. But the prioritization has often been reduced to a number-crunching exercise, where different groups give scores to different topics, the numbers are added up and voila - you have a matrix. The outcome of this process can vary widely depending on which voices you count, what weight you give to each voice, how each voice assesses the value of each impact and the weighting factors you use to roll that up into one coherent list of issues. These details are rarely disclosed by companies. The entire basis upon which material impact reporting rests is therefore not transparent and possibly, not robust.

Lloyds Bank publishes a Materiality Report.

The bank describes its process for defining material impacts:

This looks like an invested process. A universe of 50 issues was established. Representatives of six stakeholder groups (including employees as one group) took part in an online survey to rank the issues in order of importance. The online input was supplemented by the opinions of Lloyds external Stakeholder Advisory Group who provided "proxy representation on behalf of some of these groups". The responses were weighted according to "stakeholder group sample and data quality with priority given to direct feedback and Stakeholder Advisory Panel feedback". Then it was all rolled up into a set of 14 issues in 5 categories that appear to have equal priority as the most material impacts.

This looks like an invested process. A universe of 50 issues was established. Representatives of six stakeholder groups (including employees as one group) took part in an online survey to rank the issues in order of importance. The online input was supplemented by the opinions of Lloyds external Stakeholder Advisory Group who provided "proxy representation on behalf of some of these groups". The responses were weighted according to "stakeholder group sample and data quality with priority given to direct feedback and Stakeholder Advisory Panel feedback". Then it was all rolled up into a set of 14 issues in 5 categories that appear to have equal priority as the most material impacts.

The issues look to be a reasonable mix of what we might expect a large banking group to prioritize at a general level. But they could also be the issues of any bank anywhere in any country. Trust in business, job creation, access to products and services, customer satisfaction - this tells me nothing about Lloyds Banking Group that is specific to that company. This begs the questions: How detailed was the initial universe of material issues? How was the weighting of stakeholder responses constructed?

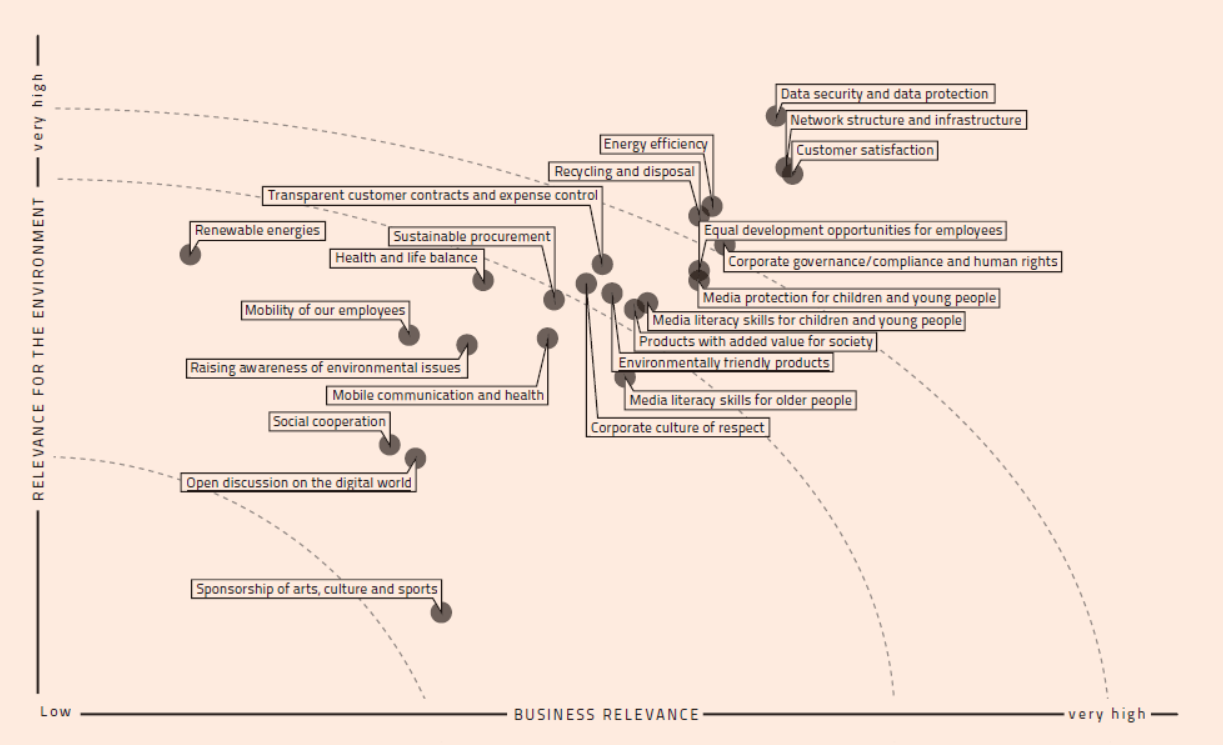

Another bank, for example, presents a more company-sector specific picture. Westpac Australia's materiality matrix includes impacts such as positive impact finance, financial capability and empowerment, digital product and service transformation (an issue which is sweeping the banking industry worldwide for obvious reasons) and macroeconomic and demographic trends that are current in the materiality assessment period.

The issues look to be a reasonable mix of what we might expect a large banking group to prioritize at a general level. But they could also be the issues of any bank anywhere in any country. Trust in business, job creation, access to products and services, customer satisfaction - this tells me nothing about Lloyds Banking Group that is specific to that company. This begs the questions: How detailed was the initial universe of material issues? How was the weighting of stakeholder responses constructed?

Another bank, for example, presents a more company-sector specific picture. Westpac Australia's materiality matrix includes impacts such as positive impact finance, financial capability and empowerment, digital product and service transformation (an issue which is sweeping the banking industry worldwide for obvious reasons) and macroeconomic and demographic trends that are current in the materiality assessment period.

Westpac's matrix refers to impacts that are important to stakeholder and important to the business, but, despite this bank's detailed disclosure of stakeholder issues and responses, we are still left in the dark about the process used to assign prioritization to these top 18 material impacts. What influenced the positioning of the dots on this matrix? How were the different stakeholder inputs evaluated?

Next week, I will be presenting the findings of an analysis I performed on behalf of BSI, the UK's national standards body, of sustainability performance and reporting standards that are used predominantly today. The presentation will serve as a basis for dialogue at an event hosted by BSI to consider where standardization or additional focused guidance may assist companies in advancing sustainability performance and reporting.

If materiality is central to reporting, does the process of defining materiality not merit greater structure and transparency? Good process, good outcome. But what is the process for determining materiality? Every company uses its own logic to develop a process that delivers a result. But if the process is flawed, then the result is flawed. How can we know that companies are reporting the most material issues? If the process is different in every case, the outcomes are not comparable. One of the recommendations I am tabling for discussion next week is that there should be robust process standards for the determination of material impacts. What do you think? I'd welcome your thoughts as we consider this fundamental question that goes to the heart of relevant corporate transparency. The actual event is fully booked with a long waiting list, so if you have a strong view, write to me here or comment on this blog. I am very interested to hear your views.

In the meantime, the good news is that companies are making efforts to define material impacts. Even an imperfect, undisclosed process is a start. As I often say, 80% of something is better than 100% of nothing.

elaine cohen, CSR consultant, Sustainability Reporter, HR Professional, Ice Cream Addict. Author of Understanding G4: the Concise Guide to Next Generation Sustainability Reporting AND Sustainability Reporting for SMEs: Competitive Advantage Through Transparency AND CSR for HR: A necessary partnership for advancing responsible business practices . Contact me via Twitter (@elainecohen) or via my business website www.b-yond.biz (Beyond Business Ltd, an inspired CSR consulting and Sustainability Reporting firm). Need help writing your first / next Sustainability Report? Contact elaine: info@b-yond.biz